With the deepening of global economic integration, more and more Chinese enterprises are seeking cross-border investment to expand their business and acquire resources, which brings about tax issues arising from the distribution of earnings of foreign enterprises as dividends to Chinese shareholders. This article takes Chinese enterprises' direct investment in the U.S. as an example, and analyzes how to make reasonable planning for the equity structure in order to reduce tax risks and improve tax efficiency.

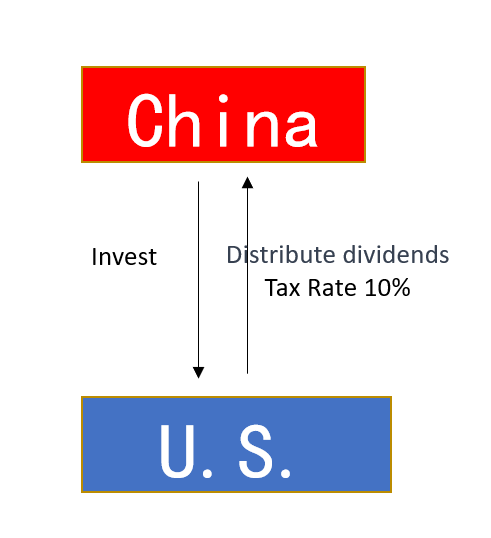

I. Direct Control Structure

Direct control structure means that the Chinese enterprise as a shareholder directly establishes a U.S. company. The advantage of this structure is that it is simple to operate and easy to manage, but it may face a higher dividend tax rate.

According to Article 9 of the Agreement between the Government of the People's Republic of China and the Government of the United States of America for the Avoidance of Double Taxation and the Prevention of Fiscal Evasion with respect to Taxes on Income, "Dividends paid by a company resident in one Contracting State to a resident of the other Contracting State may be taxed in the other Contracting State. However, such dividends may also be taxed in the Contracting State of which the company paying the dividends is a resident in accordance with the laws of that Contracting State. However, if the recipient is the beneficial owner of such dividend, the tax imposed shall not exceed 10 percent of the total amount of such dividend." Under this agreement, the tax rate borne by the U.S. company on dividend distributions to Chinese shareholders is 10%. Thus, under this structure, the advantages to the investor are a simple shareholding structure and ease of management, but a higher tax burden.

II. Indirect Control Structure

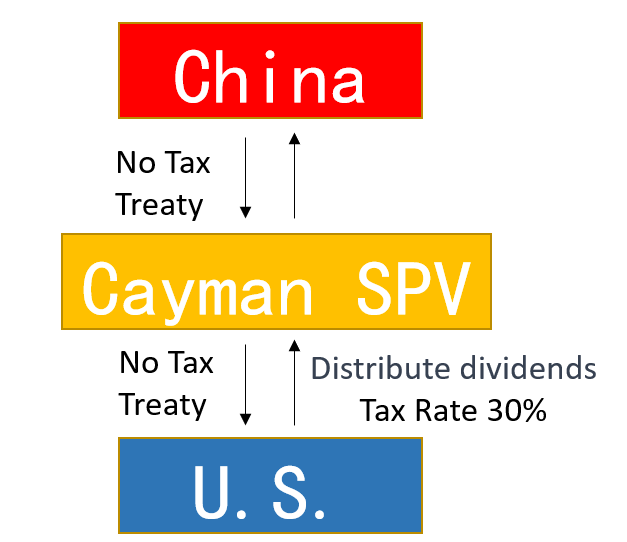

(i) Indirect investment in the U.S. through the Cayman Islands

In this structure, Chinese enterprises indirectly hold U.S. companies by setting up an SPV (Special Purpose Vehicle) in the Cayman Islands.

The Cayman Islands is a well-known offshore financial center, and its tax incentives allow companies to reduce tax costs. However, since the U.S. and the Cayman Islands have not signed a tax agreement, and the U.S. levies a 30% dividend tax on countries that have not signed a bilateral tax agreement, the establishment of an offshore company through the Cayman Islands will not save tax, but even more counterproductive, and you need to bear a higher tax burden. Therefore, when making an investment, it is necessary to fully consider the domestic laws of the investment target, bilateral and multilateral agreements and treaties, and special territorial preferences in order to choose the appropriate equity structure.

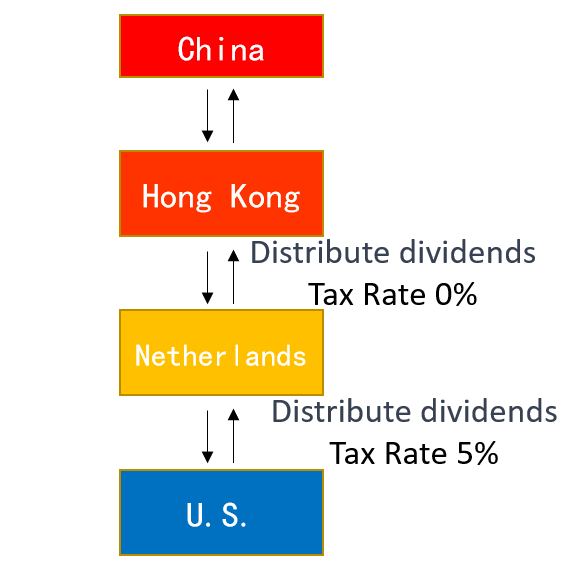

(ii) Indirect investment in the U.S. through Hong Kong and the Netherlands

In this structure, a Chinese company indirectly holds a stake in a U.S. company through the establishment of a Hong Kong company and a Dutch company. The advantage of this structure is to take advantage of the tax arrangements or agreements between China, Hong Kong, the Netherlands and the U.S., as well as Hong Kong's "territorial source taxation principle", in order to achieve tax optimization.

1. Under the Convention between the United States of America and the Kingdom of the Netherlands for the Avoidance of Double Taxation and Prevention of Fiscal Evasion with respect to Taxes on Income, the United States of America and the Kingdom of the Netherlands are required to adopt the "territorial source principle" for tax optimization. Taxation and Prevention of Fiscal Evasion with Respect to Taxes on Income), Article 10(2), a corporation is only subject to a 5% tax rate on dividends if the beneficial owner is a corporation that directly holds at least 10% of the voting rights in the corporation that pays the dividend. Therefore, when a US company distributes profits to shareholders of a Dutch company, it is only subject to a 5% dividend tax.

2. Article 10(3) of the Agreement between the Hong Kong Special Administrative Region of the People's Republic of China and the Kingdom of the Netherlands for the Avoidance of Double Taxation and the Prevention of Fiscal Evasion with respect to Taxes on Income provides for exemptions from dividend tax

Among the above five scenarios, it is easier for a general investor to establish a shareholding entity in Hong Kong to satisfy the conditions set out in item 5, which can be summarized as "the need to have business substance in Hong Kong". According to section 15K of the Hong Kong Inland Revenue Ordinance ("IRO"), the "business substance requirement" under this section is satisfied in accordance with Article 10(3)(e) of the Hong Kong-Netherlands Tax Treaty, and the Dutch company will be entitled to a "business substance requirement" when distributing profits to its shareholders in Hong Kong. A Dutch company is not subject to dividend tax on distribution of profits to shareholders in Hong Kong.

3. According to section 26 of the Hong Kong IRO, dividends can be excluded from taxable income in Hong Kong, therefore, a Hong Kong company is not required to pay dividend tax when distributing profits to Chinese shareholders.

Through the above tax arrangements or agreements among the four places and the provision of no dividend tax in Hong Kong, the equity structure can be made to have high tax advantages, but its structure has more levels and its operation and management are relatively complicated, and it is necessary to take into account the specific provisions of the tax laws and regulations of each country and the tax agreements.

III. Summarization

To summarize, for the structure planning of Chinese enterprises' direct investment in the U.S., they should choose an investment structure suitable for them according to the actual situation, taking into full consideration of various factors such as tax cost, operation convenience and tax risk. Direct holding of U.S. companies is suitable for enterprises with high requirements for operational convenience; the establishment of offshore companies and multi-level shareholding structure has higher tax advantages, but the operation and management are relatively complicated. In actual operation, enterprises need to conduct specific analysis based on their industries, investment objectives, capital size and other factors to choose the best investment structure to ensure that their investment plan complies with the laws and regulations of each country, while minimizing tax risks and costs.