Overseas investment by Chinese enterprises has shown a rapid growth trend, and Germany, as Europe's largest economy and technology powerhouse, has been an important investment destination for Chinese enterprises. When investing in Germany, many legal and tax issues need to be considered, especially when it comes to equity structure planning, which requires extra caution. In this article, we will discuss the considerations for Chinese enterprises in the planning of equity structure for direct investment in Germany from a tax perspective, in order to obtain the best tax optimization.

I. Direct Control Structure

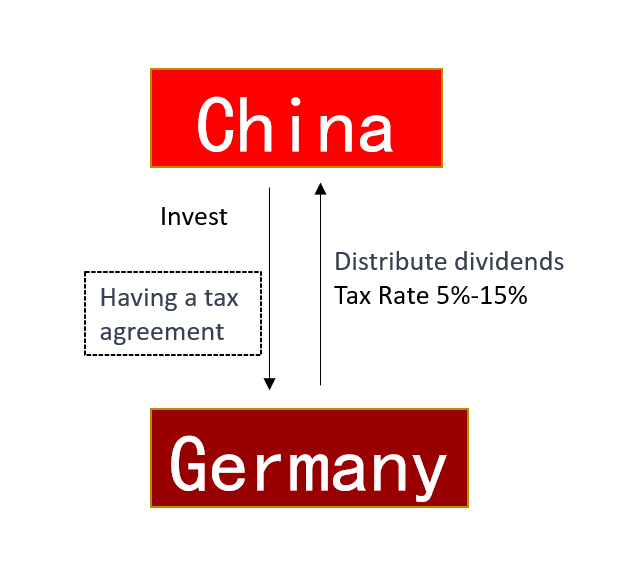

Direct control structure means that the Chinese enterprise as a shareholder directly invests in the establishment of a German company. The advantage of this structure is that the shareholding structure is straightforward and simple, and only needs to set up a company in Germany, but may be subject to a higher dividend tax rate.

According to Article 10 of the Agreement between the People's Republic of China and the Federal Republic of Germany for the Avoidance of Double Taxation and the Prevention of Fiscal Evasion with respect to Taxes on Income and Property, "Dividends paid by a company which is a resident of one of the Contracting States to a resident of the other Contracting State may be taxed in the other Contracting State. However, such dividends may also be taxed in the Contracting State of which the company paying the dividends is a resident in accordance with the laws of that Contracting State. However, if the beneficial owner of the dividend is a resident of the other Contracting State, the tax imposed: (i) shall not exceed 5 percent of the gross amount of the dividend where the beneficial owner is a corporation (other than a partnership) that directly owns at least 25 percent of the capital of the corporation paying the dividend; and (ii) where the income or gain on which the dividend is paid is derived by an investment vehicle, directly or indirectly, from an investment in immovable property subject to Article VI. shall not exceed 15% of the total amount of the dividend in the event that the investment vehicle distributes the majority of said income or gains on an annual basis and its income or gains from said real estate are exempted from tax; and (iii) in other cases, shall not exceed 10% of the total amount of the dividend." According to this agreement, the tax rate borne by the German company when distributing dividends to Chinese shareholders is categorized into 5%, 10% and 15% depending on different circumstances. Thus, the advantages of this equity structure for investors are simple shareholding structure and easy operation and management, but if the condition of 5% dividend tax rate cannot be met (more than 25% direct shareholding by legal person shareholders), a higher tax burden will be borne.

II. Indirect control structure

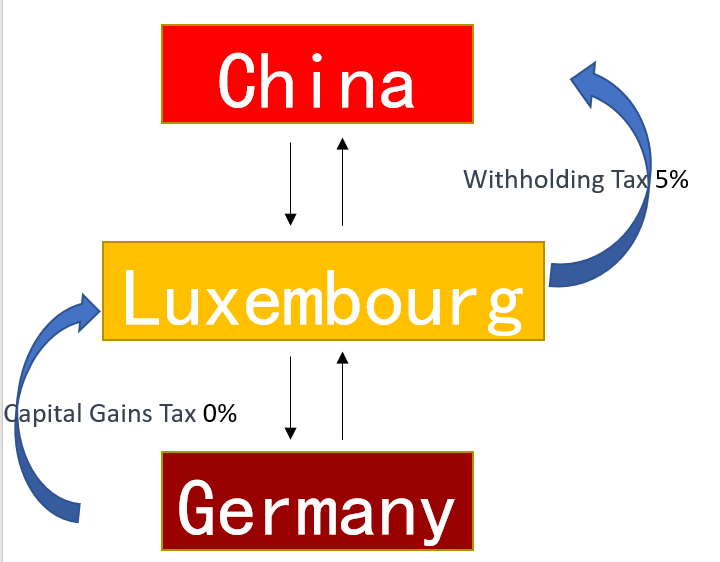

(i) Indirect investment in Germany through Luxembourg

In this structure, a Chinese company takes indirect control of a German company by setting up a company in Luxembourg.

Luxembourg is one of the six founding members of the European Union, with a strong banking and investment fund industry, and one of the largest wealth management centers and reinsurance centers in the Eurozone. The flexible and diverse regulatory and legal environment, the well-developed infrastructure of financial services and support functions, and the extremely attractive tax regime provide a unique environment for companies to set up and grow in Luxembourg, as well as to explore the EU market. Better tax optimization can be achieved through the tax policy of EU economic integration, Luxembourg's domestic tax law and the tax agreement between China and Luxembourg.

1. According to the EU Parent-Subsidiary Directive of 2011 (on the common system of taxation applicable in the case of parent companies and subsidiaries of different Member States), in the EU subsidiaries or permanent establishments in the EU are not subject to withholding tax in their country of residence when distributing dividends and profits to parent companies located in other EU Member States. Since Germany and Luxembourg are both EU countries, a German company is not liable for tax when distributing profits to Luxembourg shareholders. It should be noted, however, that in order to avoid abuse of the above directive, the EU amended the Parent-Subsidiary Directive in 2015 to allow member states to ignore artificial arrangements that are made for the purpose of tax evasion, i.e., to require that there be economic substance in the member state of the company (an arrangement or a series of arrangements shall be regarded as not genuine to the extent that they are not put into place for valid commercial reasons which reflect economic reality). Under Luxembourg tax law, economic substance is considered to be present in Luxembourg if the following conditions are met: (1) the principal officers of the company must reside or work (for tax purposes) in Luxembourg; (2) the principal management decisions must be taken in Luxembourg, and the annual general meeting of the company must be held in Luxembourg at the place of incorporation at least once a year; and (3) the company is not recognizable for tax purposes in any other country.

2. According to the Luxembourg tax law, dividends received by a Luxembourg holding company from its investee (the payer) are exempt from corporate income tax and municipal business tax if the following conditions are met: (1) the parent company directly or indirectly controls more than 10% of the equity interest of the payer or the amount of the holding is more than EUR 1.2 million; (2) the abovementioned holding has been in place for more than 12 months at the time of payment of the dividend by the payer; and (3) the payer is domiciled in an EU countries. Therefore, the Luxembourg company is not required to pay corporate income tax in Luxembourg on the income derived from the distribution of profits of the German company.

3. Article 10 of the Agreement between the People's Republic of China and the Grand Duchy of Luxembourg for the Avoidance of Double Taxation and the Prevention of Fiscal Evasion with Respect to Taxes on Income and Property stipulates that "Dividends paid by a company resident in one of the Contracting States to a resident of the other Contracting State may be taxed in the other Contracting State. However, such dividends may also be taxed in the Contracting State of which the company paying the dividends is a resident in accordance with the laws of that Contracting State. However, if the recipient is the beneficial owner of the dividend, the tax imposed: (i) shall not exceed 5% of the total amount of the dividend if the beneficial owner is a company (other than a partnership) that directly holds at least 25% of the capital of the company paying the dividend; and (ii) shall not exceed 10% of the total amount of the dividend in other cases." Therefore, if a Chinese shareholder holds more than 25% of the shares of a Luxembourg company, he or she will only be subject to a 5% tax liability when accepting profit distributions from the Luxembourg company.

The tax benefits can be better reached through the above mentioned tax arrangements for EU economic integration and tax agreements between the three countries, etc.

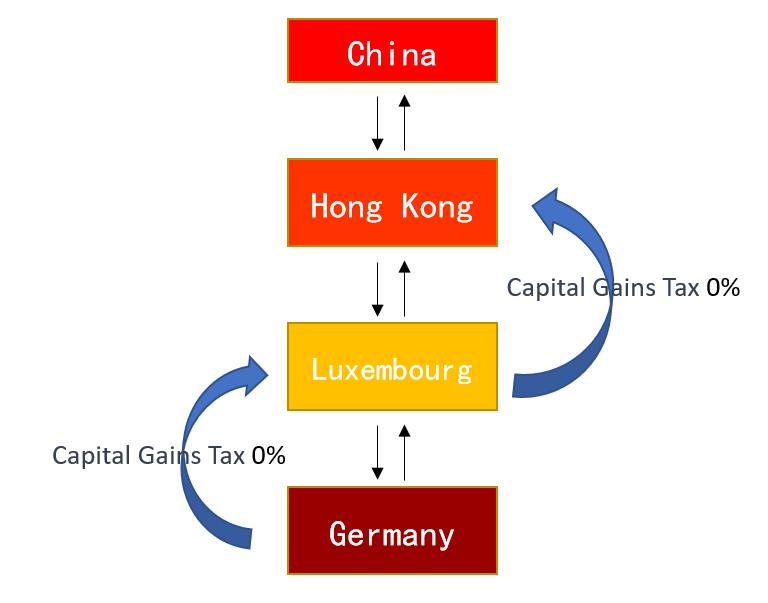

(ii) Indirect investment in Germany through Hong Kong region and Luxembourg

In this structure, Chinese enterprises indirectly hold German companies through the establishment of Hong Kong companies and Luxembourg companies. The advantage of this structure is to take advantage of the intra-EU and Luxembourg domestic tax incentives and tax arrangements or agreements between China, Hong Kong and Luxembourg, as well as the Hong Kong "territorial source taxation principle", in order to achieve tax optimization.

1. Based on the above, the distribution of profits by the German company to the Luxembourg shareholders is not subject to tax and the Luxembourg company is not subject to corporate income tax in Luxembourg in respect of such income, subject to the requirement of economic substance, due to the fact that they are both members of the European Union.

2. Article 10(2) of the Agreement between the Hong Kong Special Administrative Region of the People's Republic of China and the Grand Duchy of Luxembourg for the Avoidance of Double Taxation and the Prevention of Fiscal Evasion with respect to Taxes on Income and on Capital provides for the exemption of dividends from taxation as follows: "Where the company supporting the dividends is a resident of a Contracting Party, the said dividends may also be taxed in that Contracting Party in accordance with the laws of that Contracting Party, provided that, where the beneficial owner of the dividends is a resident of another Contracting Party, the said dividends may also be taxed in that Contracting Party under the laws of that Contracting Party. However, if the beneficial owner of such dividends is a resident of another Contracting Party: (a) where such beneficial owner is a company (other than a partnership) and where such beneficial owner directly holds at least 10% of the share capital of the company supporting the dividends or holds a right to participate at a cost of at least EUR 1,200,000, the tax so charged shall not exceed 0% of the total amount of such dividends.". Therefore if a Hong Kong based company directly holds more than 10% of the shares of a Luxembourg company or has paid not less than €1,200,000 for the acquisition of a shareholding in a Luxembourg company, it will not be liable for tax when receiving a distribution of profits from the Luxembourg company.

3. According to Article 26 of the Inland Revenue Ordinance of Hong Kong, dividends can be excluded from taxable income in Hong Kong, therefore, a Hong Kong company is not required to pay dividend tax when distributing profits to Chinese shareholders.

Through the above tax arrangements or agreements among the four places and the provision of no dividend tax in Hong Kong, the equity structure can be made to have high tax advantages, but its structure has many levels and its operation and management are relatively complicated, and it is necessary to take into account the specific provisions of the tax laws and regulations of each country and the tax agreements.

III. Examples of structures

In 2019, Jifeng, a listed A-share company, acquired approximately 80% of the equity of Grammer, a leading German manufacturer of automotive parts, by means of indirect shareholding through a Luxembourg company.

Jifeng shares, through its subsidiary JIYE Investment, firstly set up a wholly-owned subsidiary JIYE (Luxembourg) directly abroad, and JIYE (Luxembourg) invested in the establishment of JIYE (Germany), which holds the shares of Grammer Germany as the main body of direct shareholding. The above arrangement is a structure formed after comprehensively considering factors such as investor introduction, financing and control structure, tax planning and acquisition plan, which can better protect the interests of Jifeng shares.

Summary

To sum up, when Chinese enterprises invest directly in Germany, they need to take into full consideration of the tax laws of each country or region, mutual tax agreements and the EU Parent-Subsidiary Directive, etc., and choose the appropriate investment structure and tax planning, so as to minimize the tax burden, improve tax compliance, and realize the maximum benefits of investment while avoiding risks.